Infrastructure investing has always been about predictable cash flows, long asset lives, and defensible positions. For decades, that meant toll roads, pipelines and utilities. The energy transition added a new category — renewables — but largely on the same terms: one asset, one revenue stream, one risk profile.

Hybrid infrastructure breaks that logic. Not by being more complex, but by being more complete.

The single-value trap

Most infrastructure assets are optimised for one purpose. A wind farm generates electricity. A weather station collects data. A carbon project monitors emissions. Each does its job well — but each requires its own deployment, its own maintenance cycle and its own commercial relationship.

For an investor, that means three separate bets on three separate markets. Three teams. Three sets of counterparty risk. And three assets that, individually, may not meet return thresholds in a period of rising capital costs and compressed yield expectations.

The question worth asking is not which of these is the best investment? but why are we treating them as separate at all?

Most infrastructure assets are built to do one thing well. The next generation is built to do several things at once.

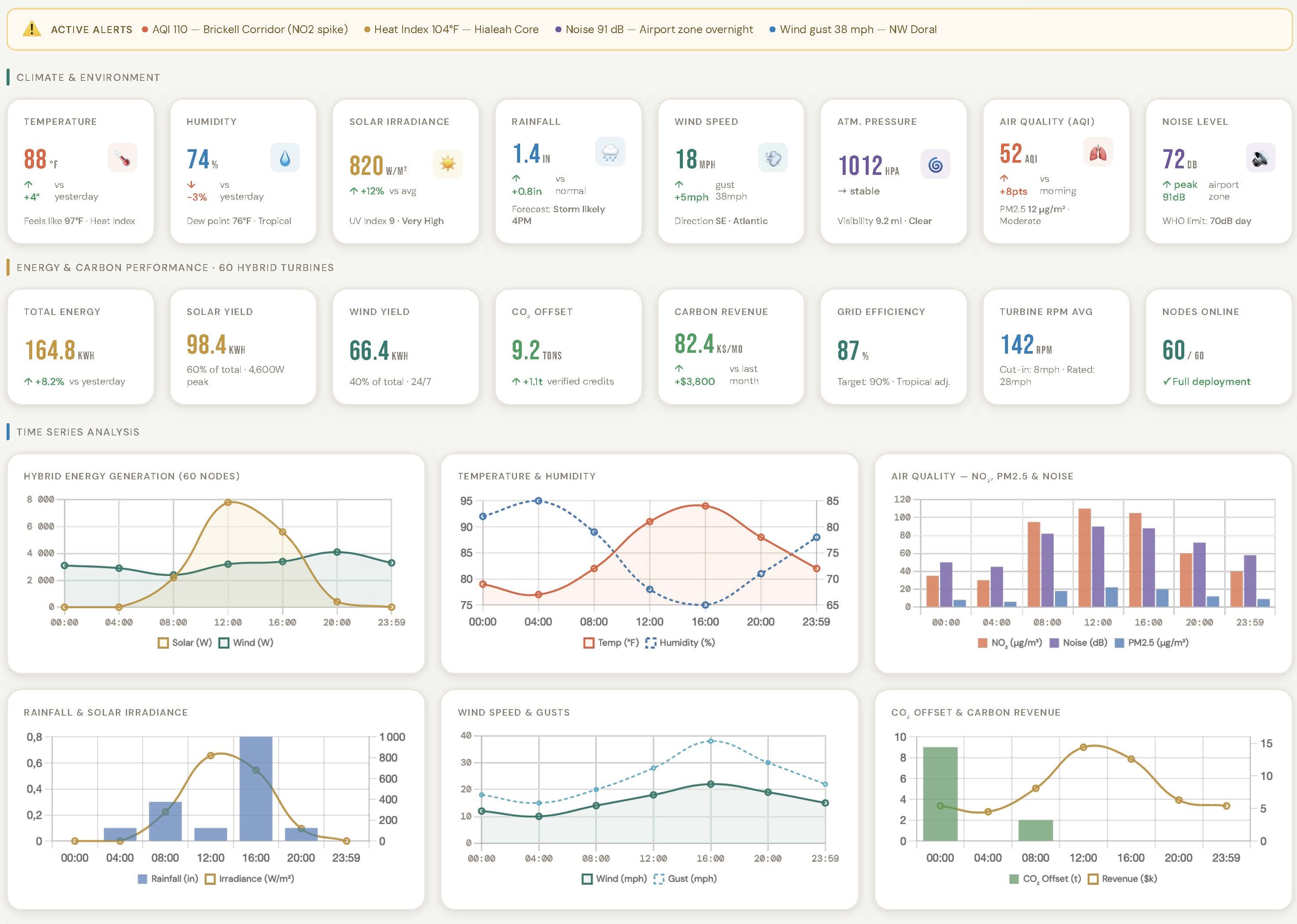

One physical footprint, four value streams

A properly designed hybrid infrastructure asset — combining distributed wind and solar generation with an embedded environmental sensing layer — can generate value across four distinct vectors simultaneously from a single deployment.

Energy production

On-site generation reduces grid dependency and creates either direct revenue through a feed-in model, a local power purchase agreement, or avoided cost for the host asset. In off-grid or weak-grid environments, this alone can justify deployment.

Resilience infrastructure

Distributed generation at the asset level — a port, a hotel, a logistics platform, a public facility or an industrial site — changes the risk profile of that asset. It is no longer fully exposed to grid outages, energy price volatility or supply chain disruption. For an infrastructure investor with exposure to operational assets, this is a hedge embedded in the physical layer.

ESG and carbon evidence

Each unit of distributed generation produces measurable reductions in electricity-related emissions. When measurement is structured properly, the same physical asset can also support audit-ready reporting, carbon accounting and certification workflows. ESG visibility is not an add-on. It becomes a direct output of the infrastructure itself.

Certifiable Gold Standard carbon credits

This is the argument few hybrid players can make. Every kilowatt-hour of locally produced renewable energy — continuously documented by on-board sensors — corresponds to a measurable, timestamped tonne of CO₂ avoided that is certifiable under the Gold Standard framework by an accredited third party.

The distinction between certifiable and certified matters: credits are not issued automatically. They are generated through a verification process that the operator can trigger when appropriate. On the voluntary carbon market, a Gold Standard-certified tonne of CO₂ trades between €80 and €120. Velox shares 50% of these credits with the site operator or client. Over a 20-year horizon, for a site producing several dozen avoided tonnes per year, this is a structural revenue stream added on top of energy production — with no additional capital expenditure.

Environmental data

The sensing layer embedded in a hybrid asset captures continuous field data: wind speed, temperature, humidity, air quality (CO₂, PM2.5), atmospheric pressure and solar irradiance. At a single site, this is useful. Across a network of deployed assets spanning multiple geographies and climate zones, it becomes something else: a proprietary real-world dataset with standalone commercial value.

That value is not abstract. Insurers need micro-climate data to price physical risk. Real estate asset managers under CSRD can no longer rely on regional estimates — they need certifiable measurements at site level. Cities building climate MRV infrastructure need sensor nodes deployed where citizens live and work. These are structural buyers, not marginal clients.

Why this matters now

Three structural shifts make hybrid infrastructure particularly relevant for investors, public authorities, asset owners and industrial operators.

The ESG data deficit is becoming a pricing problem

Asset owners are increasingly asked to report on the environmental performance of underlying assets — not only at portfolio level, but at site level. Infrastructure that generates its own environmental evidence reduces reporting friction and gives decision-makers a more reliable view of operational reality.

Distributed generation is moving from niche to necessary

Energy security has returned to the strategic vocabulary of corporate and public sector asset owners. Sites that can demonstrate partial on-site autonomy are better positioned against grid instability, electricity price volatility and continuity-of-service risk.

Data as infrastructure is underpriced

The market values data businesses at software multiples and infrastructure businesses at yield multiples. A hybrid asset that generates both creates a structural valuation ambiguity. An asset that produces a certified, continuously updated environmental dataset across a distributed network is not just an energy asset. It is data infrastructure with physical defensibility.

The compounding effect

What distinguishes hybrid infrastructure from a portfolio of separate assets is not the sum of its parts. It is the compounding effect of deploying multiple value streams through a single operational unit.

Each new site added to a hybrid network does not just add capacity. It adds a new node to the data layer, increases the density and geographic coverage of the environmental dataset, and creates another source of measurable operational and environmental performance. The network becomes more valuable as it scales in ways that no single-purpose asset can easily replicate.

For an infrastructure investor, this has a concrete implication for the risk/return profile. A conventional asset has an essentially static return: it produces what it produces, on the market it is positioned in, with few levers for intrinsic improvement once deployed.

A hybrid asset within a growing network operates on an inverse dynamic. Each additional deployment enriches the value of existing deployments — through dataset densification, improved predictive models, and growing credibility with institutional data buyers. The return on the first asset deployed improves structurally over time, without additional capex on that asset.

This asymmetry — entry risk comparable to a conventional energy asset, but optionality on data and carbon value that appreciates with scale — is not typically reflected in standard infrastructure valuation models. Early deployment positions therefore carry real optionality that the market underprices today.

A different question to ask

The standard infrastructure due diligence question is: what does this asset produce, and at what price?

For hybrid infrastructure, the better question is: how many markets does this asset participate in simultaneously, and what happens to its value as each of those markets matures?

Energy transition. ESG disclosure. Climate data commercialisation. Distributed resilience. These are not adjacent trends. They are converging — and the infrastructure assets best positioned for the next decade are those designed to sit at the intersection of all four.